5 Applications of Blockchain in Business and Economy

The blockchain is a digital ledger of transactions that records all the exchanges of cryptocurrencies in a decentralized manner. Blockchain allows the digital information to be distributed over a network without the need of any centralized mechanism. This technology was devised by a person or a group of people known by the pseudonym, Satoshi Nakamoto. Originally created to empower the cryptocurrency, Bitcoin, this technology has now become a center for innovation. But the meaning of blockchain is still not clear to every person. Here we will discuss the meaning of blockchain and the ways to leverage it.

Blockchain - Meaning and Current State:

To understand blockchain you need to first understand a block. A block is a ledger that records some part or whole of a transaction. For a transaction to be recorded it needs to be verified by nodes (computer connected to blockchain network). Once recorded, it cannot be altered which brings security and stability in the blockchain. To verify a transaction every node needs to solve a complex problem and in return of solving that problem, it is rewarded with bitcoins.

Every block contains the hash of the previous block. Each time a block is completed it is linked to the previous block and a new block is created. This forms a chain of blocks that are known as blockchain. Thus, a blockchain contains records of all the transactions from the most recent to the oldest. All the information in blocks is encrypted to prevent any alterations to the data. Cryptography ensures that the information in the blocks can be distributed but not copied.

Read More: Bitcoin vs Blockchain - What is the difference?

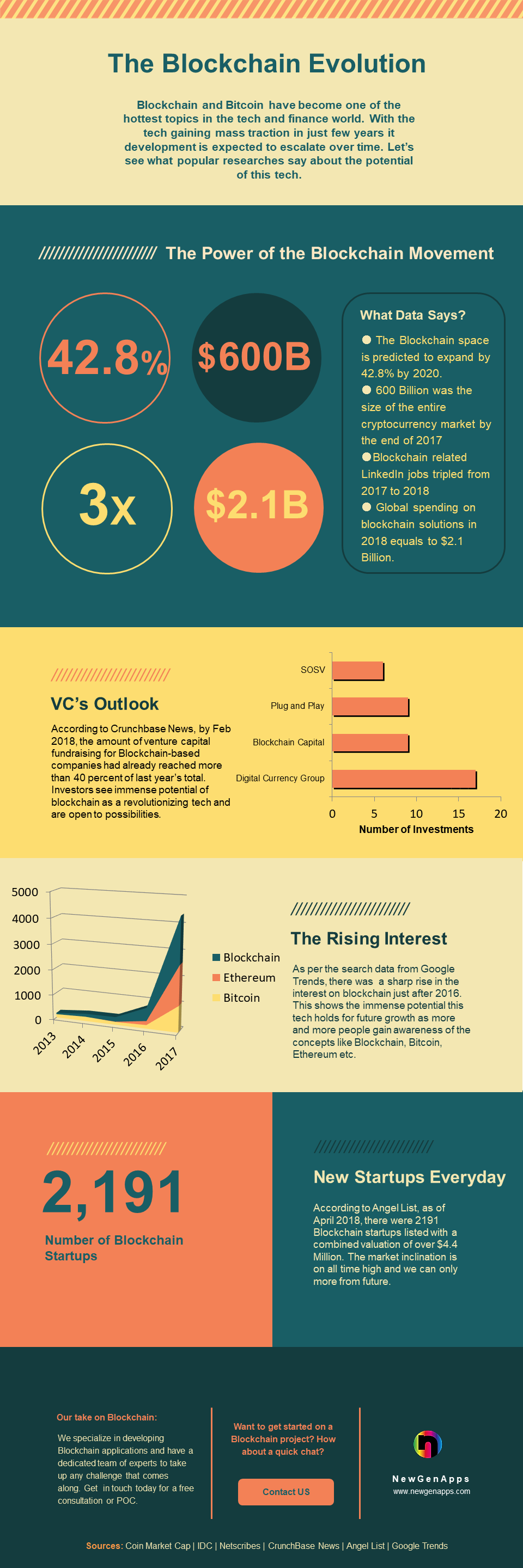

Feel free to use this infographic. Just give us a mention.

Share this Image On Your Site

Please include attribution to NewGenApps with this graphic.

5 Applications of Blockchain Technology:

The most common application of blockchain is obviously in cryptocurrencies. There are 100s of cryptocurrencies like Bitcoin and Ethereum that leverage blockchain to successfully complete transactions. Here are some other applications of blockchain apart from cryptocurrencies:

1. Finance:

Traditionally to transfer money from one person to another we needed an intermediary. That intermediary ensured that the money is safely transferred from one end to another. The dependency of the intermediary increased proportionally to distance and value of the transaction. These intermediaries are called banks. With the help of blockchain, it is now possible to eliminate these intermediaries and decentralize the transactions. Bitcoin is the most popular application of this blockchain. If applied on scale blockchain can make transactions easy and simple.

For instance, claims processing in insurance can be a cumbersome process. Insurance processors manually go through fragmented data sources about client’s history, financial conditions etc. This makes the entire process time consuming and prone to errors. The blockchain provides a risk-free and transparent solution to the problem. Its encryption properties allow insurers to know the ownership of insured assets and the financial history of the insured person.

Read More: Impact of Bitcoin on the Economy

2. Cloud Computing:

In the present scenario cloud storage services are centralized — i.e. you the user must place trust in a single cloud storage provider. That storage provider has control over all your online assets. It also difficult to migrate from one provider to another. With the help of blockchain, it is possible to provide decentralized storage solutions thus, mitigating the risks with cloud storage. Anyone on the internet can store your data at a pre-agreed cost. The data security is ensured by having multiple copies over the network.

Storj.io and Factom are two start-ups exploring this idea. Storj is a beta-testing cloud storage solution, leveraging blockchain technology to decrease dependency while ensuring data security. The data is encrypted and then sent out to the network. Basic metadata is used to keep the track of data. You can consider this technology as the Airbnb of data storage.

Read More: 11 Experts on the Future of Blockchain Finance

3. Smart Contracts:

Smart contracts are legally binding programmable digitized contracts created using blockchain. Legal contracts are implemented as variables and settlements can be made using bitcoin network instead of relying on a centralized source. Blockchain can bring in a digital revolution in the legal industry. Whether it a divorce settlement or a mortgage case, lawyers are excellent in creating tons of paperwork. This is done primarily to hide the information or delay opposition from finding valuable insights.

Blockchain can help digitize the process of keeping track of the paper trail and reduce the costs and chances of errors. Firms like Stampery, have started a shared ledger that works as an irrefutable digital proof of a legal event that happened between two parties. This could be anything from a real estate case to a divorce proceeding, basically anything that involves digital proofs.

Read More: How to raise funds for a blockchain app?

4. Logistics and Asset Management:

Tracking is the core of any logistics activity. It helps in ensuring the products are safely transferred within the estimated time frame. Real-time tracking and monitoring have always been the goal for logistics companies. But tracking assets in real time is a real challenge. It requires appropriate storage, tracking mechanism, network etc. To avoid problems, companies usually rely on checkpoint tracking i.e. to track the movement from one checkpoint to another. Blockchain can now make it possible to track assets in real time. The current systems only allow tracking the product’s serial number and value. The blockchain ledger is so dynamic that now you can not only track the location but also other information like destination, people involved, tax, and government clearance, etc.

Read More: 5 uses cases of Blockchain beyond Finance

5. Internet of Things (IoT):

IoT is the interconnectivity of non-IT devices to a network. Internet of things enables you to monitor and control devices remotely. With blockchain in the picture, now these devices can be shared across a network. Blockchain can maintain a record of activities in the network and help a common device be used by multiple people. For example, smart cars can be bought in the pool and can be used by many people easily. This will enable a more advanced and community level usage without the need for human intervention.

The blockchain is enabling community level usage of many things like solar panels, wastewater catchment systems etc. Reputation protocols can help determine whether it is fit to offer community services to an individual or not. By recording the usage by different individuals in the network it will be easier to determine fair rates of exchange, creating a transparent and equitable framework for resource allocation. This model is more energy efficient because people will only for their exact usage.

Read More: Experts on How Blockchain can Secure the IoT

The blockchain is a vast field and there are many possible applications. If used properly it can help in rapid development in many industries. If you are looking for blockchain developers then feel free to contact us:

{{cta('f9c16880-daa3-4732-af3e-83158cf8740a','justifycenter')}}